Frequently Asked Questions for Maryland Candidates - 2017 Version of the Uniform CPA Examination - CPA Examination - Public Accountancy

When will the next version of the CPA Examination launch?

The next version of the Uniform CPA Examination will launch on April 1, 2017 (the second administration window of 2017).

How many sections will the next version of the CPA exam include?

The next version of the CPA examination will have the same four sections as it does now:

- Auditing and Attestation (AUD)

- Business Environment and Concepts (BEC)

- Financial Accounting and Reporting (FAR)

- Regulation (REG)

What’s new about the new CPA exam?

Exam Methodology

The CPA examination will put more emphasis on the assessment of candidates’ higher-order cognitive skills. There will be more task-based simulations (TBSs). The TBSs will require candidates to solve practical simulations by analyzing and evaluating situations, applying accounting principles,and creating and implementing processes and procedures. To understand this method of testing, see Bloom’s Taxonomy of Learning Domains.

Testing Duration

To accommodate the TBSs, the duration of the Business Environment and Concepts (BEC) and Regulation (REG) sections of the CPA Examination will be increased from 3.0 hours to 4.0 hours. Each of the CPA examination section will be 4.0 hours long.

Rest Breaks

When the new version of the CPA examination is launched on April 1, 2017, candidates will be entitled to a 15-minute break at about halfway through each section. This 15-minute break will not count against the four-hour time allocated to complete the section. A candidate can accept or decline to take the break at the midway point. Candidates will not be able to defer the “free” midway break until later in the testing period. Candidates may take additional breaks that will count against the testing time at any time.

More Days of Testing

Ten additional days of testing have been made available for candidates to schedule an examination section. Candidates are able to schedule exams during the first ten days of June, September, December and March. Forty additional test days will be available each year, with the exception of June 2017, the first administration window after the launch of the new version of the examination.

Tell me more about testing higher level thinking skills!

The AICPA has developed examination blueprints that discuss the content, skills and typical tasks that are contained in each section of the CPA examination. The blueprints provide greater clarity in the presentation of content, skills and related representative tasks that may be tested. The blueprints contain approximately 600 representative tasks across all four sections, which are aligned with content and related skills required by newly licensed CPAs. View the Exam Blueprint.

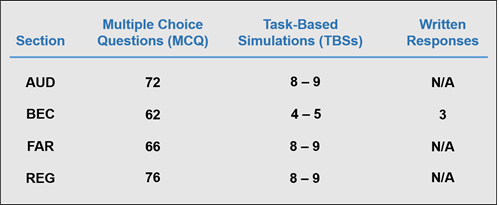

What types of items will appear on the next exam?

Candidates will be assessed on a variety of content using multiple-choice questions (MCQs), task-based simulations (TBSs) in all four sections (including Document Review Simulations (DRS) discussed below). The BEC section will also include three written responses.

How are the items distributed on the next exam?

Scoring weights for AUD, FAR and REG will be approximately 50% MCQ / 50% TBS. Scoring weights for BEC will be approximately 50% MCQ, 35% TBS and 15% written response.

Will the Document Review Simulation (DRS) be included on the next exam?

Beginning with the 2016 Q3 testing window (July 1, 2016), the current exam will use a new simulation item type known as the Document Review Simulation (DRS) in the AUD, FAR and REG sections. The DRS will continue to be used after the launch of the next exam where it will be added to the BEC section as well. DRS samples can be viewed in the exam sample tests.

Will I still get credit for passing sections of the current exam after the next exam launches?

Any combination of passed current exam sections and passed exam sections after April 1, 2017 will count toward licensure. All candidates will take the next version of the CPA exam sections beginning in the second quarter of 2017. Thus, any sections passed prior to the launch of the next exam in the second quarter of 2017 will count toward licensure requirements (subject to the 18-month rule) going forward.

How soon will I get my scores with the next exam?

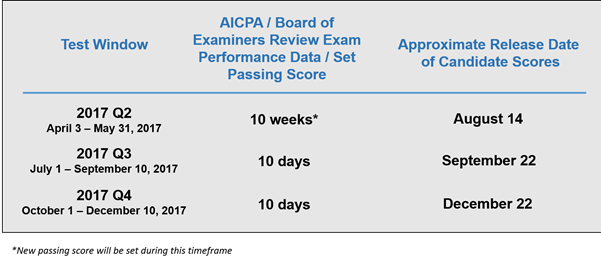

The changes in the exam will not impact the existing average 20-day score release timeline on an ongoing basis. However, consistent with exam launches in the past, there will be a delay in the release of scores following the close of the initial testing window (second quarter of 2017). Scores will be released once, approximately 10 weeks after the close of the testing window. For the third and fourth quarters of 2017, scores for all candidates will be released once, approximately 10 days after the close of each testing window. The delay in score releases for the Q2, Q3 and Q4 testing windows provides sufficient time to statistically validate candidate performance on the next exam. In the first quarter of 2018, it is expected that the existing average 20-day rolling score release timeline will resume.

What kind of information will be provided on the score report?

What kind of information will be provided on the score report?

The design and content of the candidate’s score report have not yet been determined.

How do I appeal my score under the next exam?

The score review and appeal process remains the same under the next exam.

How much will it cost to take the next exam?

Implementation of the exam in 2017 will require fees for the BEC and REG sections to be modified to reflect the additional testing time from 3.0 hours to 4.0 hours. The Board has not determined the amount of the fees at this time.

Other resources for questions about the changes in the CPA exam

For content questions about the exam, please visit the AICPA website.

For questions related to the administration of the exam, please visit the NASBA website.